Buy vs. Rent in India: The Simple Financial Math Every Indian Needs to Know

Should you buy a home or rent and invest the money instead? This is one of the biggest money questions for Indians — whether you live in Jaipur, Mumbai, Delhi, Bengaluru, Hyderabad, Pune, Chennai, Kolkata, Ahmedabad, or Surat. The answer is not the same for everyone. Let's break it down simply.

City-Wise Reality Check: Buy or Rent?

Property prices and rental costs are very different across Indian cities. Here's a quick look at what you're dealing with:

Jaipur: Property rates in Vaishali Nagar, Malviya Nagar, or Mansarovar range from ₹40–80 lakh for a 2BHK. Monthly rent for the same flat: ₹8,000–15,000. Rental yield is only about 1.5–2% — one of the lowest in India. This makes renting very attractive in Jaipur.

Mumbai: Even a 1BHK in the suburbs costs ₹80 lakh–1.5 Cr. Renting is nearly always cheaper in the short term.

Delhi NCR: Prices in Noida and Gurugram have risen sharply. Renting in Dwarka or Greater Noida can save you ₹30,000–50,000/month vs. EMI.

Bengaluru: IT hub with high demand. Areas like Whitefield and Sarjapur have good rental demand, but prices are rising fast.

Hyderabad: One of the more affordable metro cities. Rental yields in Gachibowli and HITEC City hover around 2.5–3%.

Pune: Popular with IT and manufacturing workers. Renting in Hinjewadi or Kothrud is a smart short-term option.

Chennai: Stable property market. Rental yields in OMR and Velachery are around 2–2.5%.

Kolkata: One of the most affordable metros. Buying in Salt Lake or New Town can make sense for long-term residents.

Ahmedabad: Fast-growing city with reasonable property prices. SG Highway and Satellite area offer value for buyers.

Surat: Business-driven city with strong rental demand in textile and diamond trade areas.

The Real Cost of Buying a Home

When you buy a home, you pay much more than just the property price. Here's what actually goes out of your pocket:

Down Payment: Usually 20% of the price. For a ₹60 lakh flat in Jaipur, that's ₹12 lakh upfront.

Stamp Duty & Registration: In Rajasthan (Jaipur), stamp duty is around 6% for women buyers and 7% for men — that's ₹3.6–4.2 lakh on a ₹60 lakh home.

Home Loan Interest: At 8.75% for 20 years, you end up paying nearly double the loan amount in total.

Maintenance & Society Charges: ₹2,000–5,000/month ongoing.

Property Tax: Paid every year to the local body (like Jaipur Nagar Nigam).

The Real Cost of Renting

Renting is not 'wasting money' if you use the saved amount wisely. Here's what renting gives you:

Flexibility: Easy to shift cities or neighbourhoods for a better job or lifestyle.

Lower Initial Cost: No large down payment needed. Your savings stay invested and keep growing.

Zero Maintenance Tension: The landlord bears the cost of repairs and upkeep.

More Monthly Cash: Your EMI would be much higher than your rent in most Indian cities.

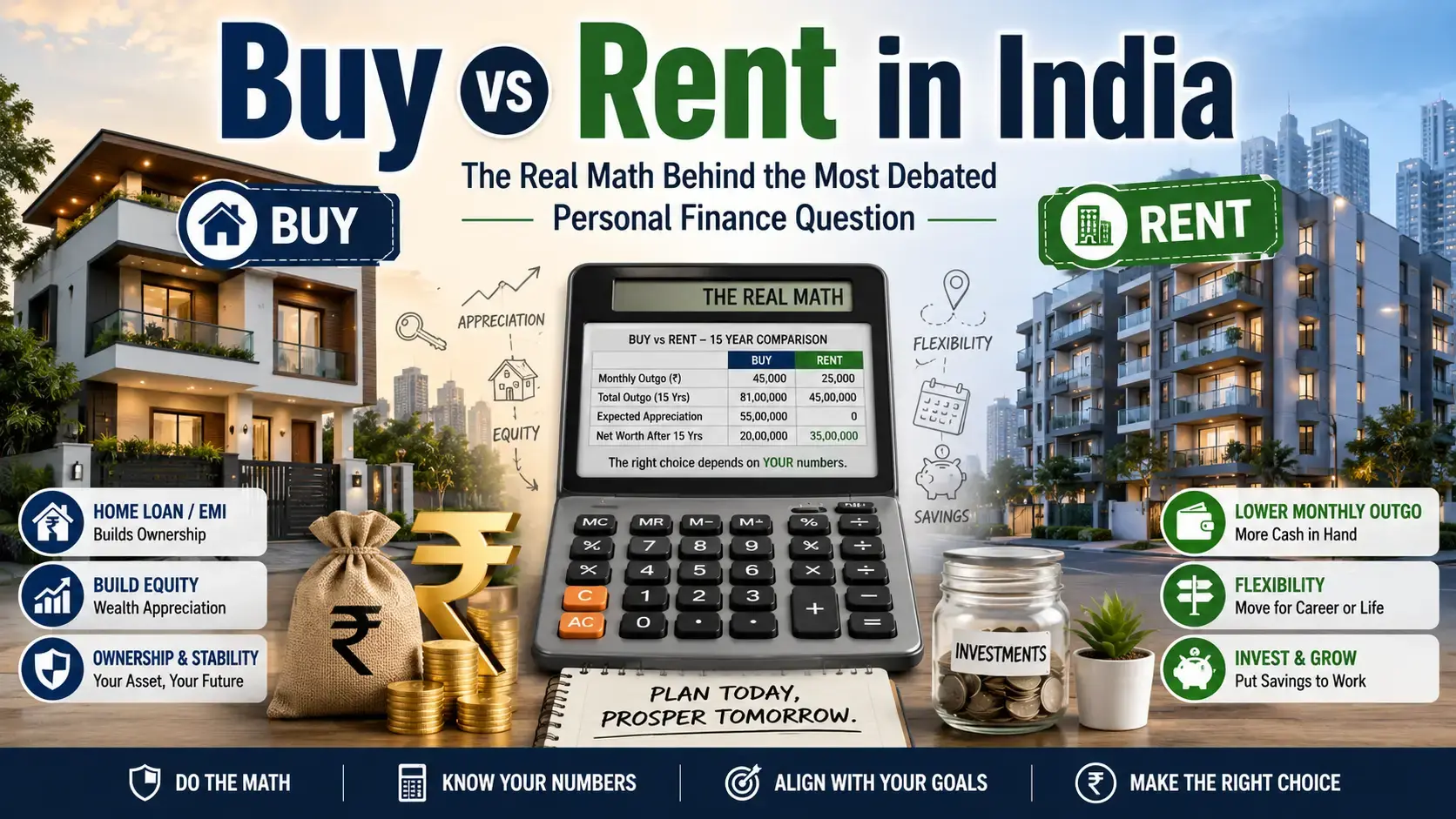

The 'Invest the Difference' Strategy — A Jaipur Example

Let's make this real with a simple Jaipur example:

A 3BHK flat in Vaishali Nagar, Jaipur costs ₹80 lakh.

Home loan EMI (₹64 lakh loan at 8.75% for 20 years): approximately ₹56,000/month.

The same flat on rent: approximately ₹15,000/month.

Monthly difference you can invest: ₹41,000

If you invest ₹41,000/month in an index mutual fund earning 12% per year, in 20 years you could have over ₹3.8 Crore — which is likely more than the property itself would be worth after accounting for all costs.

Use our Buy vs. Rent Calculator to run this math for your own city and budget.

When Does Buying Make Sense?

You plan to live in the same city for at least 10 years (Jaipur, hometown, etc.).

You have the 20% down payment ready and your emergency fund is untouched.

You want the emotional security of your own home and the freedom to renovate it.

You're in a city like Kolkata or Ahmedabad where prices are still relatively affordable.

You want a fixed living cost for retirement planning.

When Does Renting Make More Sense?

Your job might require you to move — especially in IT, government, or defence sectors.

You're in a city like Jaipur or Mumbai where rental yields are very low (under 2.5%).

You're comfortable investing in mutual funds or stocks and want to maximise your wealth.

You are under 35 and still building your career and savings.

Property prices in your target area are too high compared to local salaries.

Key Numbers to Know Before You Decide

Price-to-Rent Ratio: Divide the property price by the annual rent. Above 20 means renting is better. In Jaipur, a ₹60 lakh flat renting at ₹12,000/month gives a ratio of 41 — strongly in favour of renting.

Rental Yield: Annual rent ÷ property price × 100. Under 2.5% means renting is cheaper than buying.

Break-Even Period: How many years before buying becomes cheaper than renting? In most Indian metros, it's 12–18 years.

Conclusion

There is no one right answer for everyone. A person in Jaipur with a stable government job may find buying a home very sensible. A young IT professional in Bengaluru or Hyderabad who may shift cities in 3 years should probably rent and invest. The key is to run the numbers honestly and match them with your life plans. Don't let social pressure push you into the biggest financial decision of your life.

FAQs

Q: Is renting a waste of money in Jaipur?

A: No. In Jaipur, rental yields are around 1.5–2%, which is much lower than home loan interest rates of 8.5–9%. If you invest the money you save vs. an EMI in a mutual fund SIP, you can often build more wealth over 15–20 years.

Q: What is rental yield and why does it matter?

A: Rental yield = Annual Rent ÷ Property Price × 100. In India, most cities have yields of 2–3%, while home loan rates are 8.5–9%. This gap is why renting and investing is often the smarter financial choice.

Q: What is the 2% rule in real estate?

A: If the annual rent is less than 2% of the property value, it is usually better to rent than to buy. Most Indian cities including Jaipur, Mumbai, and Delhi fall below this threshold.

Q: Should I buy a flat in Jaipur right now?

A: It depends. If you're planning to stay for 10+ years and have a stable income, it can be a good decision. But if you're likely to move or if the EMI will strain your monthly budget, renting and investing the difference is the smarter move in 2025–26.

Q: Which Indian cities are best for buying property?

A: Cities with relatively affordable prices and good appreciation potential — like Ahmedabad, Jaipur (some micro-markets), Kolkata, and parts of Hyderabad — currently offer better value for buyers than Mumbai or Delhi NCR.

Related Tools

Finance Disclaimer

This content is for educational purposes only and should not be considered financial advice. Please consult a certified financial advisor before making investment decisions.